Look, I know it’s fashionable to rant about the “algorithms” and how they are brainwashing us by feeding us pointless nonsense. Experts peoples tell me that by giving us what we want, the “algorithms” are turning our brains into mush. It’s a ploy by the overlords that control these algorithms to make us docile enough to control us , like puppets. In our anthropomorphized descriptions of algorithms, they are akin to Darth Vader and Moriarty. But damnit, once in a while, the algorithms feed us something really good.

The good thing the algorithms fed me this week was this wonderful conversation between the amazing John Cleese and the incredible Stephen Fry. I loved it. Maybe it’s because they are British, and there’s something about British accents—they seduce you, titillate you intellectually, and make you mentally moist.

John Cleese and Stephen Fry talk about many things, from cricket, money, and work to artificial intelligence. But the part of the conversation that I loved the most was about money—it was beautiful. There was nothing in it that you and I didn’t know about, but sometimes it takes a British accent to make us think that the obvious is profound.

Like most Indians, I grew up in a family that swung between abject poverty and a luxurious lower-middle-class lifestyle. The thing about childhood experiences is that they leave a deep imprint on us. In my journey of learning about money, a revelatory moment was when I learned that our lived experiences tend to leave long-lasting scars, thanks to Ulrike Malmendier, a professor of economics and finance at the University of California, Berkeley. Our lived experiences shape everything, from how people perceive risk to their job choices, consumption patterns, and more. It sounds obvious, but sometimes the obvious things sound like profound realizations because we ignore them because they’re obvious. I wrote a little about the long lasting scars that early experiences leave on us a few months ago when Silicon Valley Bank committed hara-kiri. A couple of weeks ago, I learned about the neurobiological basis for why early experiences leave a lasting imprint on us, thanks to neuroscience professor Robert Sapolsky.

Early experiences have lifelong and even multi-generational effects. It's essential to understand that an individual's environment doesn't start at birth; a significant portion of it is shaped during the prenatal period. The impact of early-life experiences can be enduring, stretching across generations, and this is especially true for early childhood adversity. While some of its effects can be mitigated through adult intervention, the longer one waits to address them, the more challenging it becomes to reverse their impact.

Your early experience is going to cause lifelong changes in your brain, which will make you more likely to reproduce the same early experience for your offspring.

Coming back to the point about money, it’s a peculiar object. In a utilitarian sense, it’s the single most uncomplicated object in life: money is a means to an end. But emotionally, boy, oh boy, is it complicated! Money can evoke a million emotions, from love, hate, and envy to shame, disgust, and misery. I can’t think of any other object or experience that can conjure up such a bhelpuri of emotions—not even the first memory of your lover’s kiss or the classical Greek sculpture of a naked rhinoceros.

Coming back to the previous point about early experiences, we are all forever tainted by the beliefs of your family and friends about money. Beliefs about money are like social pathogens. They infect our minds when we are growing up because we are blank slates. No matter what we do or how old we become, we’ll never get rid of the pathogens—there’s no vaccine. Like addicts battling addiction, we’ll have a lifelong struggle with what money means to us. Our own beliefs about money will always be anchored to those of the people around us growing up, and most of us won’t even realize it.

One reason I loved this conversation is because Stephen Fry was honest about how he thinks about money. Like most people, I have a complicated relationship with money, and listening to the conversation was a reminder to keep reminding myself about what’s important and what’s not.

The other reason I wanted to share this is because money is the single biggest cause of stress among people. Just because our beliefs about money are shaped by so many things and people doesn’t mean we accept them. We may never have the perfect relationship with money. I don’t think so, because it’s so interwoven across all facets of our lives. Money is a part of most of our life decisions; it’s everywhere, like dark matter causing a tug in our behavior.

But.

You can get to a place where you have a functional relationship with money. It’s like if you are addicted to weed, you don’t keep it at your house but at your friend’s place. You just go there and smoke once a week. You figure out ways to deal with the nauseating and dizzying range of emotions that money causes. Even Robert Sapolsky, who thinks we have no free will, says we can change:

All of this can instill a wonderfully positive belief: that change can occur, even in the face of trauma or the most challenging circumstances. It reminds us that change is possible, that things can evolve. We should not adopt a fatalistic mindset or believe that, because we are mechanistic biological beings without free will, we cannot change ourselves. Instead, we can be transformed by our circumstances.

So, while we acknowledge that change can be incredibly difficult or seemingly impossible and that circumstances can change us, striving to be better human beings remains a worthwhile pursuit. The key is recognizing that change can happen within the framework of our mechanistic neurobiology, making us more receptive to optimism and less susceptible to discouragement.

To change, you need to ask the right questions, and for that, you have to read, listen to other people’s experiences, and think.

Stephen Fry: We're none of us entirely wide-eyed and naive about the world; we know that about the world, and it has always been the case that money talks and that everybody has a price to some extent.

John Cleese: Do you know what Napoleon said?

Stephen Fry: No, go on.

John Cleese: He said the surprising thing is not that every man has his price but how low it is. I think that's hilarious.

Stephen Fry: I've always thought the greatest power a human being can have in negotiations, whether it's as an actor in a film as minor as that or in a huge, boardroom way, is the power to walk away. Yeah, just to be able to say, Oh no, this is not for me, and go.

John Cleese: Have you ever understood why people want to be so rich? We all want to be able to have a better bottle of wine, or we all want to have a nice car, or maybe a slightly bigger house, but I think the point of being very rich is to be able to tell people that you are very rich.

Stephen Fry: Essentially, I think it is a display. It's very fashionable these days to look into genetics and ancestry and to picture our ancestors in a cave or in a field, you know, hunting and gathering, and we know that some part of being human is acquisition, is territorial acquisition, and whether it's land, building a castle like this, as a display as well as a defense, and money is a defense as well as a display. It protects you from everything in the world.

John Cleese: Why such huge sums of it?

Stephen Fry: You join a sort of club in which, you know, people in the suburbs might say they've got a better lawnmower than I have. I'm going to have to upgrade my lawnmower. I'm going to have to upgrade my strimmer. All the sort of suburban things, keeping up with the Joneses, we call it. It's a very...we've talked about that all our lives. We know it as a phenomenon. But you scale it up. You simply scale it up. And we know this is true. I mean, I can still picture the moment when I was nine and I found an old Macintosh, an old raincoat people used to wear them, and it had a 10 Shilling note in it, and the joy, yeah, the absolute joy. Now what you can't do is scale that joy up. If I then found £100,000 in a coat, I would be astonished. I would go, "Wow," but I wouldn't be...um...well, 10 Shillings is, you know, half a pound, so I wouldn't be 200,000 times happier than when I found that 1 note.

John Cleese: But people think more is better, don't they? I mean, alcoholics think more is better.

Stephen Fry: There are many aspects of humanity where we are bound, if we're honest, to inspect ourselves and say, "I get that. I feel like that." But also, "I don't feel like that." I've always been very lucky with alcohol, for example. I do like a drink. I like wine. But I know I could never be an alcoholic. I just don't like it enough. I don't like feeling sick. I don't like having to cope with the responsibility of apologizing the next day if I've been drunk. I don't like the fact I might get a bit argumentative. So I just, you know, could never be an alcoholic. But I could be lots of other things that I do recognize faults in. Andsimilarly with money. I mean, I like having enough money. I'll be honest to turn left on an airplane. I think it's the most...I still get excited by it. I still think, "Oh my goodness, I'm going first class," and I love it. I mean, I just love it, and it's a disgrace, and I know I shouldn't. And I try and do this keyword carbon offsetting.

John Cleese: You used the keyword "enough." So these very rich people have no sense of enough. Can you understand it? I mean, it's an illness.

Stephen Fry: It is an illness.

Stephen Fry: I was born in the same year as Sugar Puffs, the cereal, right? So I... I should never forget. Yeah, I was of a generation for whom television advertising was first directed towards me when I was young, to eat Sugar Puffs and Rice Krispies and Frosties and sugary things. And I went to a school which had a Tuck Shop, you know, a little boarding school, and there were things like sherbet fountains with sherbet in it, white powder that you... you sucked in through a licorice straw. And they even extraordinarily had Spanish gallant rolling tobacco, which was coconut shreds, but it was done exactly like a rolling tobacco packet that you'd see grown-ups using, and you would have a pipe made of licorice, uh, and you would have cigarettes with red tips on the end, which were candy cigarettes. Do you remember all these sweets?

Well, you're probably a generation older. You didn't have quite... No, there was a... But they were so... You were being prepared for cocaine and tobacco, essentially. You were given white powder and tobacco, and I never could eat enough of that, and I would break out of school bans, go to the village shop, and buy all the fruit salads and Black Jacks and foamy shrimps and little rice paper flying saucers, and I stuffed myself. I couldn't eat them. I... I got teeth missing here because of it.

So I... I had this empty hole in me, this vast empty hole that said, "Feed me. I need this sugar. I need it." And then when it wasn't sugar, it became tobacco, and I smoked. And then in my 20s, it became cocaine. I just... And I couldn't sit still without going, you know, and it's that addictive impulse that many people, many people watching will know what I mean. And many people won't because this is the important thing to remember. I said, "Not everybody has this." And it's a kind of addictive gene. And I guess the money people have it for money. There's this hole in them they have to acquire and they have to own.

John Cleese: They don't know how to fill it, no. And they think if I had another 500 million, I'd be happier.

Stephen Fry: One of the things that always maddened me about self-help books and books on there is the ones that start off with "Goal orientation, set yourself goals." And I think it's the most dangerous and despicable, inimical thing imaginable because I don't know a human being who, when they reach a goal they've set themselves, isn't dissatisfied. Absolutely always an anticlimax.

The other thing I remembered as I was writing this was the book Balance. It’s a wonderful book about personal finance that I read recently. I had written a small review of the book as well. The key message of the book is to think about your personal finances holistically; in other words, it’s just about money. Here’s an excerpt from the book:

Plenty of people seek success, but they don’t define it holistically. To many, like my students, success means money in the bank, a great career, or a big house on the hill. How often have you heard (or even said) something like, “That woman is so successful. She owns a massive house, a BMW, and her own law firm” Unfortunately, this picture defines only one element of success: monetary. As I see it, there are four quadrants to a successful life:

Having enough money

Maintaining strong relationships

Maximizing your physical and mental health

Living with a sense of purpose

Think of success as a four-legged table, with each leg representing a quadrant. Each quadrant depends on the other. If they don’t all play their part equally, the table collapses. If one leg is spindly or cracked, it’s tough to maximize your life satisfaction, no matter how solid you might be in the other three quadrants.

Unfortunately, when defining success, we often focus too much on the money leg.

Getting to a place where you can say “enough” is a superpower. I hope to get there.

Live players

Since I wrote about the death of social media platforms last week, I gots to address the deranged ketamine-laden elephant in the room: our lord and savior, Elon Musk. Our Lord made an appearance at the New York Times DealBook Summit, and this happened when Andrew Sorkin asked him about his recent trip to Israel:

Andrew Sorkin: What was that trip like? Obviously, you know that there's a public perception that, and you're clarifying this now. But there is a public perception that that was but part of a so-called apology tour. If you will, this had been said online, there was all of the criticism, there were advertisers leaving, and we talked to Bob Iger.

Elon Musk: I hope they stop you.

Andrew Sorkin: You don't want them to advertise?

Elon Musk: No.

Andrew Sorkin: What do you mean?

Elon Musk: If somebody could try to blackmail me with advertising and blackmail me with money, go fuck yourself. Go fuck yourself. Is that clear? I hope it is. Hey, Bob. If you're in the audience.

Andrew Sorkin: Well, let me ask you then about the economics of X if part of the underlying model, at least today, and maybe it needs to shift. Maybe the answer is it needs to shift away from advertising. If you believe that this is the one part of your business where you will be beholden to those who have this view. What do you do? Linda Yaccarino is right here, and she's got to sell advertising.

Elon Musk: What this advertising boycott is is going to do is it's going to kill the company. And the whole world will know that those advertisers killed the company, and we will document it in great detail.

And then this also happened:

Elon Musk: Jonathan, the only reason I'm here is because you are a friend. What was my speaking fee?

Andrew Sorkin: I'm Andrew.

I mean, a lot has been said about this weird conversation. The way I would describe it, is a masterclass in blowing $44 billion. I don’t want to waste my time rehashing it. Also, I'm not an Elon fanboy, and I don’t care much about what he says or does. I care to the extent that he owns Twitter. I care because it’s the platform where I keep track of amazing thinkers, the latest research, and discover most of the things I read. Despite it stinking more than the open-door toilet near the majestic busstand, as someone once said, Twitter is like having the smartest people in your pocket.

It’s not a great mystery that X is in trouble. In Elon’s defense, it was decaying before his arrival, but he may have accelerated the process. Not everybody agrees; some believe Elon will magically pull a rabbit out of the hat and make Twitter better. I’m not so sanguine about that possibility, but my crystal ball is as cloudy as the next person’s.

At some level, maybe we have to care a little about what Elon does. He’s the CEO of one of the largest electric vehicle companies in the world, a rocket company, a satellite internet company, and the public toilet of the internet—Twitter (X). He’s also on a mission to spread his seed, as if he’s delivering newspapers and wants to take us to Mars after his planting season is done. So you gotta pay some attention to him—he needs it too.

Now, given his silly antics, antisemitism, and right-wing kookiness, it’s easy to dismiss him as another nutjob billionaire. But at the same time, he heads some of the most important and civilization-defining companies in the world. If you are jobless in life to worry about the contradictions and cognitive dissonance caused by our Lord and Savior, Elon, here's a frame of thinking that may help. I recently heard political analyst Samo Burja on a podcast. He talks about the idea of live players and dead players, which I think is an interesting way to think about smart but crazy people.

Here’s what a live player is:

The most basic observation is that nearly everyone is following conventions right? You follow conventions and pre-designed scripts in your life - be it through the educational process, be it following the standards of your industry - and for the most part these conventions are in place for good reasons. Right? You don't necessarily want, uh, your doctor improvising your treatment. Well, that is until you do - until you do have a rare condition that's not common and that's not well covered by the literature.

So the vast majority of society, uh, is not, uh, improvising. Right? They're not very good at coming up with new, uh, processes, new ways of doing things on the fly. Honestly, they're not even that good at evaluating evidence. There's plenty of empirical evidence for this poor quality of our ability to evaluate evidence on the fly - massive literature, uh, you know, some of it even replicates in the cognitive science field and the biases literature, and so on. Uh, but also just, you know, day-to-day experience.

So why, you know, live players - right? - people who actually are always thinking from first principles. They're remarkably rare in society. Um, but one of the best ways to sort of spot such individuals is people who easily and successfully jump multiple domains through the course of their life.

I don't think Elon's even listening. I think that Elon's perspective is so first principles-driven that while he does recognize what is popular and what is not and can work with it, his decisions as to what to do next are not tied at all to the mainstream but are following, I don't know, like, a technology tree chart derived from basic physics or his favorite science fiction story. Let's expand through the universe; let's have AI not kill us; let's actually reach a new Destiny.

Samo calls Elon a live player

Live players are basically just people who can respond to circumstances as they arise, rethinking things from first principles or just a really well-known intuition.

Dead players are people who follow a preset script. It can even be a very high-quality script, so one can easily be a dead player and still be a top performer.

Why do I frame them in terms of players? Well, because you have to think about a game. Live versus dead players is a lens that helps you think through a game. You imagine a political setting, economic setting, right? Two companies competing. Uh, who's going to win? Well identify who's the live player and who's the dead player. Why? Because you know the live player can always read the dead player's rule book and then just do something more. The dead player can't really predict what the live player will do.

In fact, live players cannot predict what live players will do. All they can do is proactively, dynamically respond to it. So if you have a competition of dead players, you look at all of their fundamentals and you bet on the one with the best fundamentals. If it's countries competing, the biggest army, the most natural resources, whatever. As soon as you introduce a live player, they might still lose, right? There's nothing really, you know, they might get taken out too early in the game.

But if you have like a fairly reasonable contender and they're a live player, the advantage is so outsized it's it's just not even, it's not even funny. I think it usually, you know, either economically, politically or in any other domain, you kind of need a live player to beat a live player and a dead player will just tend to lose.

Now this is not to say that live and dead players exist only in a zero-sum context.

I gotta agree with this brilliant piece. There' can never be a “good “social media site. Bhuvan’s law: Human nature ensures that anything that can go to shit, will eventually.

Spinning up new social media websites mimics this, except what you are trying to outrun is human nature. No design of social media can get rid of what I like to call the “semantic nadir,” which is what you’ll inevitably experience if your tweet ever goes viral, wherein eventually someone will take your tweet in literally the worst possible way (there’s some classic examples of this, as generally if you say “I love cheesecake” it won’t be long before someone reaches to “Oh, so you hate regular cake”—that’s the semantic nadir).

Good reads

There’s rampant inequality. No, there isn’t. Yes, there is.

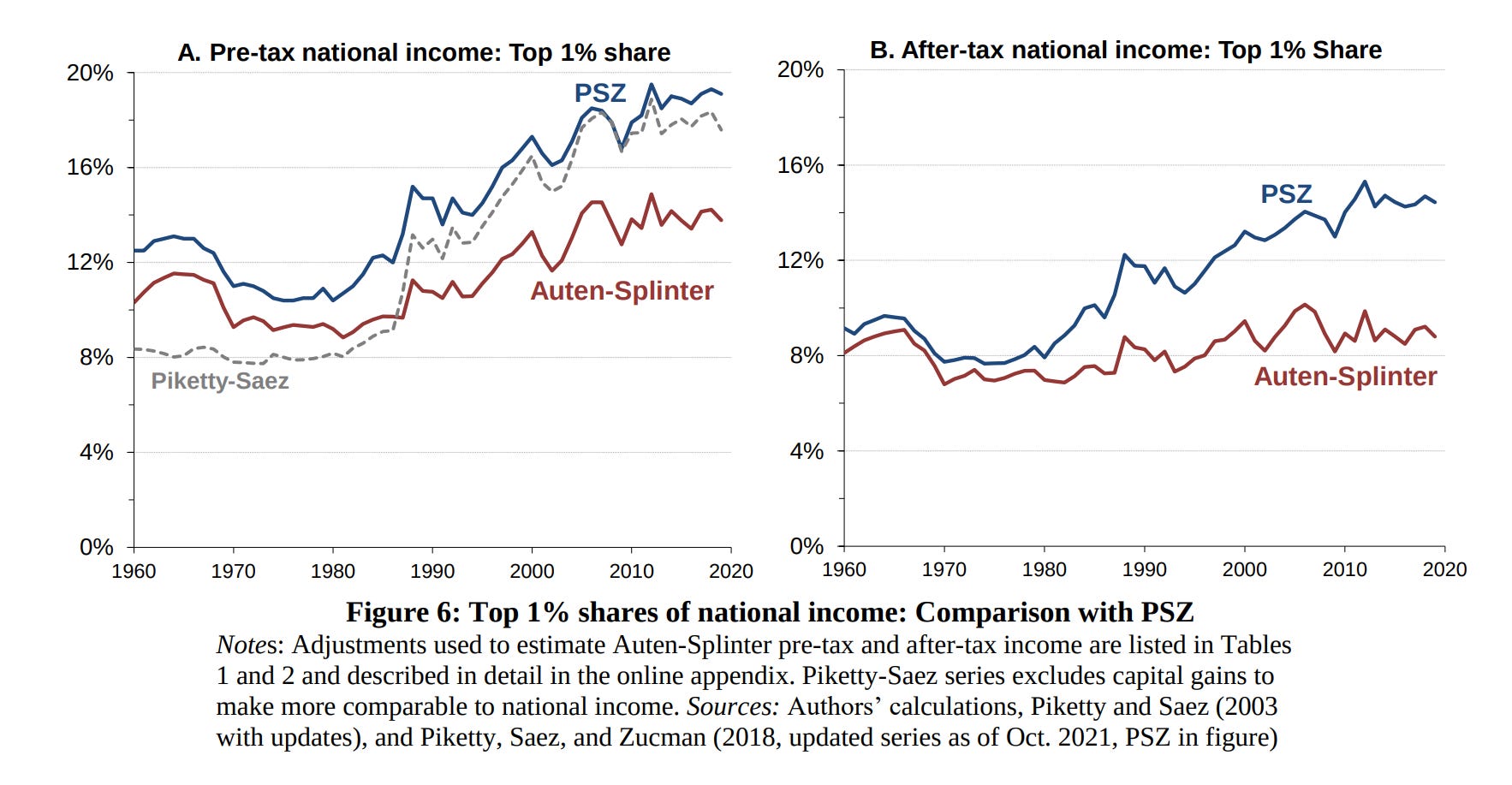

In a development that surprised everyone in the universe, from earthlings on Earth to Cyberton, Arakkis, Vogsphere, and Tatooine, economists are fighting again. Thomas Piketty, Emmanuel Saez, and Gabriel Zucman became superstars for their work showing that income inequality has exploded across much of the world.

But in 2018, economists Gerald Auten and David Splinter published a new paper using the same data as Piketty, Saez, and Zucman and came to the opposite conclusion that inequality has not exploded. Their paper was recently accepted in the Journal of Political Economy (JPE) and sparked a debate on Twitter.

So, what’s happening?

This isn’t a new debate. Piketty, Saez, and Zucman have long been accused (archive) of poor methodological choices since 2014 (archive). In their defense, they’ve engaged with the critics. But let me tell you something shocking: assessing inequality trends is hard. A lot of the arguments boil down to methodological choices and data sources because good data just isn’t available. These debates are good because they can attract other researchers to look at their issues with a fresh set of eyes and improve our understanding.

I’m not the most qualified person to assess these decisions. But there are a ton of weird decisions and adjustments regarding profits and business income that are super consequential for the conclusions drawn by AS.

You might think that analysing trends in income inequality would be straightforward. Don’t people’s tax returns tell researchers all they need to know? But although tax returns are useful, they can mislead. Americans who are partners in a company, or hold investments, often have enough trouble estimating their own income. Now imagine trying to estimate the incomes of millions of people over several decades, accounting for overhauls to the tax code. Researchers then need to account for the 30-40% of national income that is not even reported on tax returns—including some employer-provided benefits and government welfare. Researchers’ methodological choices have huge effects on the results. — Why economists are at war over inequality (archive)

I have been researching economic violence in India, where it surged during periods of social distancing and lockdowns. This not only resulted in the reduction of safe spaces for women and girls, but also trapped them in a space where they were more easily economically exploited. My research suggests that the COVID lockdowns spawned a whole new class of economic abuse of women in India.

Outside economics, Milei has also voiced support for liberalizing gun laws and greenlighting the sale of organs. Years ago, he floated a “free market” for the sale of babies, an idea he has since distanced himself from. In line with his anarcho-capitalist beliefs, Milei has pledged to cut 10 federal ministries, privatize state industries, and dismantle the public health care system in favor of private alternatives. Foreign policy wouldn’t be spared from major changes, either: Milei has suggested he would distance Argentina from Brazil and China, the country’s two biggest trading partners, and align closely with the United States and Israel.

These three cases—the commodification of books, the privatization of prisons, the commercialization of governments and universities—illustrate one of the most powerful social and political tendencies of our time, namely the extension of markets and of market-oriented thinking to spheres of life once thought to lie beyond their reach.

This economistic view of virtue fuels the faith in markets and propels their reach into places they don’t belong. But the metaphor is misleading. Altruism, generosity, solidarity, and civic spirit are not like commodities that are depleted with use. They are more like muscles that grow stronger with exercise. One of the defects of a market-driven society is that it lets these virtues languish. To renew our public life we need to exercise them more strenuously.

From fluffy interviews on YouTube podcasts with millions of subscribers to subliminal attacks on Instagram Reels, the political parties in India are betting big on influencers to swing voting patterns, manage crises, and help them secure power as the world’s largest democracy gears up for state elections this month, and a national election in 2024. It’s a strategy that makes sense—622 million Indians are online, and with the cost of internet access falling, people from India’s harder-to-reach hinterlands are coming online fast. Two-thirds of the population lives in these areas, giving them enormous power to sway the results of national elections. And while the symbiotic relationship between political campaigns and influencers has allowed politicians to reach the electorate in new ways, and to influence how they vote, it’s also helped them to dodge media scrutiny during public engagement and to challenge the integrity of elections in I had written about the scourge of influencers in the content of finance.

As the Biden administration has doubled down on the surge of additional U.S. arms and forces to the Middle East, however, it is not clear that U.S. policymakers have thought through the second- and third-order effects of amplifying the United States’ security role in the region and how it will be perceived by adversaries and allies alike. Specifically, there are three risks that the Biden administration must acknowledge and address: escalation, backlash, and overstretch.

Opec’s market-share strategy last time round helped discipline America’s oil producers, pushing them to become more efficient and therefore more resistant to future squeezes. JPMorgan Chase, a bank, reckons that the cost of getting oil out of the American ground has declined by more than one-third since 2014. The country’s oilmen have found methods to fracture rocks that produce more fissures, easing the extraction of oil, and now drill deeper wells that have longer lifespans.

The UAE guys must have seen Glengarry Glen Ross.

The United Arab Emirates’ team organizing the COP28 climate talks that begin this week was planning to use its position as host of the summit to strike new oil and gas deals with foreign governments, a cache of leaked documents shows. — CNN

This article is a transcript of a discussion on the energy transition. I’ve yet to watch the video, but I read the transcript, and it’s fascinating.

A few highlights:

Oil has become less inelastic thanks to new technologies and electric vehicles.

We may not face shortages of critical commodities required for energy transition as many people assume. Also, they are less bad than the oil industry would like us to believe. Like Indian found a massive lithium deposit, “commodities have a way of showing up when somebody needs them.”

We’re in an era of “actor less threats” like the COVID pandemic and climate change.

The world economy may be entering this mid-transition, unstable phase. This is happening even as climate impacts and other impacts of the polycrisis worsen. In this context, there’s a real risk of the world economy being increasingly exposed to cross-border risks of an economic and financial nature, which would deepen fragmentation.

In my view, the focus on winners and losers is missing a very big blind spot, which is that we’re facing a huge collective action trap related to political economy. Neither the middle classes in high-income economies nor the majority of developing economies have the means in the current international institutional configuration to achieve the transition. We are seeing the simultaneous occurrence of significant costs related to climate policies and rules of the game that prevent many countries from achieving a rapid transition. The risk is that this could give rise to a significant political backlash.

That’s why I think there’s a blind spot on this discussion about winners and losers—because we will all be losers, in an absolute sense, if the current configuration persists. That is because we are likely to see these very significant binding constraints materialize both on resources and supply chains.

There’s also the issue with China—much like a lot of other countries and particularly the US—where it is a large domestic producer of a lot of fossil commodities, but also newer energy products. This, of course, has very big macro implications for anyone who trades with China in commodities.

We see the risk of a trap because of numerous cross-border feedback loops. To give you one example, the materialization of physical climate risks hit hydropower in Latin America, directly leading to a buildup of fossil infrastructure to offset that. Multiple countries face sovereign debt crises arising from different sources, which have led to an inflow of foreign direct investment into extractive sectors to address these countries’ foreign currency needs. There are also huge gas projects in Argentina. The climate crisis will continue to be fueled by all this.

China has been building up its petroleum reserves like crazy during COVID. As soon as they stopped, the market kind of fell out of bed. In a weird way, China’s been acting like a covert central bank of oil

I think about all these discussions in terms of priorities. There’s almost no country in the world where climate change is an actual political and social priority. And if you don’t have something prioritized then you’re not going to get very much done about it.

If EVs are not affordable, you can’t leave a big chunk of the US middle class without freedom to move around.

I liked what Alex said about this convergence of interests. That’s why you see the military in the US talking about climate and security. And what Amy said—of course, it’s exactly right that you asked, what will it take to take climate seriously? War is one thing. But to go back to my point, we can use things people really care about—like security, like air and water pollution, and like economic development—as prime motivators that will help the climate as well. You can get some of these happy coalitions. But if you insist on transacting everything through a climate lens, it is, in my view, not the most powerful nor the most effective way to make those transitions.

Does reducing CO2 emissions mean sacrificing economic growth? Or can we “decouple” the two, by both growing the economy and reducing emissions?

The answer is yes: many countries have managed to achieve economic growth while reducing emissions.

You can see several examples in the chart: it shows the change in annual CO2 emissions and GDP per capita since 1990. In these countries, GDP has increased over the last 30 years while emissions have fallen. You can also see the data without per capita adjustments.

But is this all due to offshoring production overseas — transferring emissions to manufacturing economies such as China and India?

In the chart, we see that consumption-based CO2 emissions — which adjust for emissions from goods that are imported or exported — have also fallen. It’s true that some emissions have been offshored overseas, but that is not the only driver of the decline.